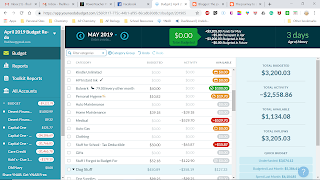

Here is what my budget looks like:

This is just like what we do every payday. We pull out $300 in cash and split it up into envelopes. Groceries get $200, Charlie gets $60, and I get $40. That's what we have until next payday. If the grocery money runs short, then Charlie will take some of his own money to cover it. So we don't look at the total amount we have, $300, we look at what is available in each envelope. So if I have $40, I can spend $40 but if I only have $20, that's all I have. OMG!!! I feel like such an idiot. It took me so long to get this. So now I have to move things around between 'envelopes' to cover this and then I will have to refill the envelopes tomorrow when we get paid. Okay, so if I'm going to pay something that I don't have an envelope for, I need to move the money from one of the other envelopes to cover it. I then have to make sure to refill that envelope when I get more money. Okay, I can live with this now - I think. Sometimes I just have to 'talk' it through to really get it in my head.